Wall Street Intelligence

Institutional-grade research and market insights reports — led by Michael Sincere, MarketWatch columnist for 20+ years and bestselling financial author.

MICHAEL SINCERE Research Analyst and Ghostwriter

Michael Sincere is one of MarketWatch's longest-serving columnists. His "Long-Term Trader" column has run for over two decades, attracting 100,000+ views per article. He is the author of 10 books published by McGraw-Hill, Simon & Schuster, and Wiley — two of which are bestsellers translated into 13 languages. He has interviewed Peter Lynch, John Bogle, Suze Orman, and Mark Minervini. He has appeared on CNBC and ABC, and produces institutional research for a leading investment bank.

At NHP, Sincere leads the editorial direction of all research and market insights reports.

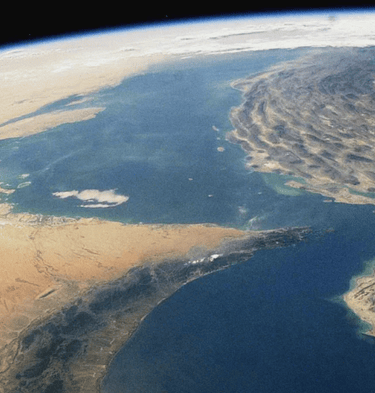

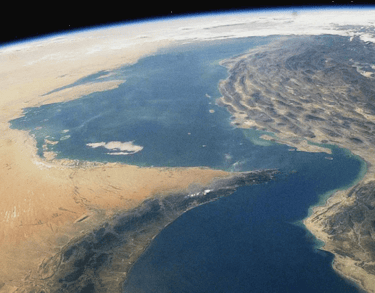

The Hormuz Crisis

How the World's Largest Energy Disruption Is Reshaping Business in the GCC-Asia Corridor

Research Report | Energy & Geopolitical Risk | Spring 2026 Published March 11, 2026

Situation Report: Day 12 of Conflict | By Michael Sincere, Deron Wagner, and Naveed Gul

KEY FINDINGS

On February 28, 2026, the United States and Israel killed Iran’s Supreme Leader. Twelve days later, 6.7 million barrels of Gulf oil production are shut in, 700 ships cannot exit the Strait of Hormuz, and JPMorgan is warning that Gulf states will exhaust storage capacity and halt production entirely by March 21. The window to act is not weeks—it is days.

This is not a market event with geopolitical overtones. It is a military conflict that has interrupted approximately 20 million barrels per day of normal Hormuz flow—far exceeding the 4.5 million bpd removed in the 1973 Arab embargo [1] and the 4.3 million bpd lost in the 1990 Gulf War [2] and confirmed by the IEA as the largest oil supply disruption in history. [3]

Brent crude hit $119.50 before retreating on diplomatic signals that have since been retracted. Iran’s new Supreme Leader has not spoken publicly. Iran’s parliament has explicitly rejected a ceasefire. There is no diplomatic framework in place.

What follows is a situation report for business operators and institutional investors with exposure to the GCC-Asia corridor. The key findings summarize where things stand. The body explains the mechanisms. The Decision Framework at the end identifies what to do now, before the next development forces a harder choice at a higher cost.

The Hormuz closure is threatening approximately 20 million barrels per day of normal flow—confirmed by the IEA as the largest oil supply disruption in history, far exceeding the 4.5M bpd removed in the 1973 Arab embargo and the 4.3M bpd lost in the 1990 Gulf War.

• Brent crude peaked at $119.50 before retreating to ~$88 on diplomatic signals. The IEA is expected to approve the largest-ever emergency reserve release (300–400 million barrels) today.

• The Strait of Hormuz is selectively closed: Iran continues shipping oil to China while blocking all other commercial traffic—a geopolitical weapon, not a blanket closure.

• GCC economies face a paradox: record oil prices they cannot monetize. Dubai’s airport, ports, and two AWS data centers in the UAE have all been damaged or disrupted.

• Asia bears the heaviest burden: South Korea’s operational LNG reserves at import terminals cover approximately nine days of normal consumption—the country’s mandatory minimum stockpile level—before drawing on strategic stocks; India’s rupee hit an all-time low; the Philippines imposed a four-day work week; Pakistan enacted its largest fuel price hike in history.

• No ceasefire in sight: Iran's new Supreme Leader (Mojtaba Khamenei) has not spoken publicly. Iran's parliament explicitly rejected a ceasefire.

Market Outlook Reports

Quarterly assessments of global equity markets, sector trends, and macroeconomic shifts.

OUR REPORTS

Indicator & Sentiment Analysis

Actionable intelligence from key technical indicators including the VIX, MACD, RSI, and moving averages.

Sector & Thematic Research

Deep dives on AI in capital markets, energy transition, GCC diversification, and geopolitical risk.

Investment Strategy Briefings

Portfolio construction, hedging frameworks, and bull/bear cycle positioning.

Custom Thought Leadership

Branded white papers and executive briefings produced for your organization.